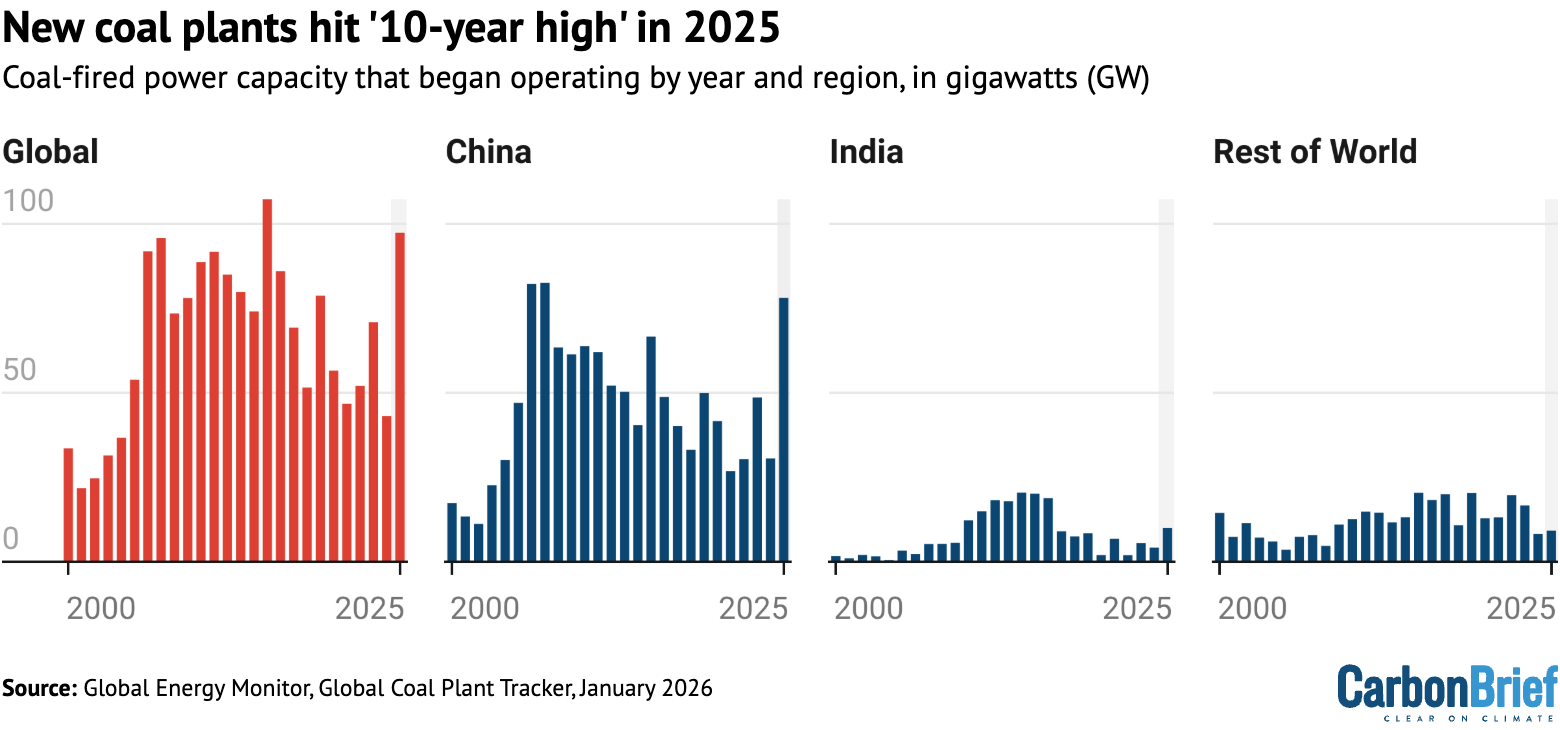

In a paradoxical development for the global energy landscape, 2025 marked a decade-high for the construction of new coal-fired power plants. According to the latest annual report from Global Energy Monitor (GEM), the world added nearly 100 gigawatts (GW) of new coal capacity—a volume equivalent to roughly 100 large-scale power stations. Yet, this surge in steel and concrete stands in stark contrast to the reality of the power grid: global electricity generation from coal actually fell by 0.6% during the same period.

This "widening disconnect" defines the current state of the global energy transition. While nations continue to commission new coal assets, the fuel’s actual contribution to the power mix is being cannibalized by the relentless, record-breaking growth of wind and solar energy. As the economics of renewables continue to improve, the world finds itself in a state of transition where the physical legacy of coal power remains stubbornly persistent, even as its functional utility begins to wane.

The Geography of Growth: A Two-Nation Hegemony

The expansion of coal in 2025 was not a global phenomenon, but rather a concentrated effort by two of the world’s largest economies. China and India accounted for a staggering 95% of all new coal-fired capacity brought online last year.

China, the undisputed leader in both coal expansion and renewable deployment, added 78GW of coal capacity, representing a 6% increase in its national coal fleet. India, following a similar trajectory, added 10GW, a 3.8% increase. In sharp contrast, the rest of the world combined added a mere 9GW. This geographic concentration underscores a fundamental shift in the coal sector: it is no longer a global growth industry, but a regional one, driven by specific national energy security policies in Asia.

However, the raw capacity numbers mask a sobering economic reality for these nations. Despite the 6% growth in Chinese coal capacity, coal-fired power generation in the country fell by 1.2%. In India, the 3.8% growth in capacity was met with a 2.9% drop in actual generation. These figures indicate that new and existing power plants are being utilized less frequently, a phenomenon that erodes the profitability of these multi-billion-dollar investments. As renewable energy increasingly captures the growth in electricity demand, these new coal plants risk becoming "stranded assets"—massive capital expenditures that struggle to compete with the near-zero marginal cost of wind and solar.

A Chronology of Conflict: Policy and Crisis

The persistence of coal is not merely a matter of industrial inertia; it is a direct consequence of geopolitical instability. The 2022 energy crisis, triggered by the Russian invasion of Ukraine, shattered the assumption that global energy markets would transition smoothly toward cleaner alternatives.

2022-2023: The Security Pivot

The sudden restriction of natural gas supplies forced many nations—particularly within the European Union—to reconsider their phase-out timelines. The "energy security" imperative prompted a scramble to retain coal capacity that had been scheduled for retirement. GEM reports that nearly 70% of coal-fired units slated for closure globally in 2025 were kept online, often due to emergency policy interventions born from the lingering fears of the 2022 crisis.

2025: The Year of the "Disconnect"

By 2025, the trend had crystallized. While the initial panic of the gas crisis subsided, the policy momentum remained. In the United States, government interventions kept aging coal plants operational through federal "emergency" orders, despite the plants’ declining competitiveness. These measures have come at a significant cost; according to GEM, these interventions contributed to a 7% rise in average U.S. household electricity prices, as consumers bore the burden of maintaining inefficient, legacy infrastructure.

The Impact of Geopolitics

The volatility introduced by the Iran war and subsequent energy market shocks in mid-2025 reinforced the "persistence of policies" that favor coal. At least eight countries announced plans to either increase coal usage or delay planned phase-outs in the immediate aftermath of the conflict. Yet, analysts note that these reactions were largely reactive and temporary, failing to reverse the long-term trend of coal’s declining share in the global energy mix.

Supporting Data: The Economics of Obsolescence

The tension between capacity and generation is best understood through the lens of data. Capacity refers to the potential maximum output of a power plant, whereas generation measures the actual electricity produced.

- Global Capacity Additions: In 2025, the world saw 97GW of new coal capacity reach operation. This is the highest level since 2015, when 107GW came online.

- The Renewable Overtake: Despite the capacity build, a report by the thinktank Ember confirms that 2025 was the year renewable energy officially overtook coal as the world’s largest source of electricity.

- The Declining Pipeline: While China and India are expanding, the rest of the world is contracting. The number of countries with new coal plants under construction or development fell from 38 in 2024 to 32 in 2025. Notable withdrawals include South Korea, Brazil, and Honduras, the latter two marking the total exit of Latin America from new coal-power proposals.

The data suggests a structural decoupling. As wind and solar continue to drop in cost, they are increasingly able to meet the entirety of new electricity demand. In China, for instance, a record 212GW of solar was added in the first half of 2025 alone, cementing its status as the nation’s largest clean-power source. When clean energy meets demand growth, coal generation is pushed to the margins, regardless of how many new plants are built.

Official Responses and Expert Perspectives

The global community remains divided on how to manage this transition. Christine Shearer, project manager of GEM’s Global Coal Plant Tracker, highlights the irony of the current situation: "In 2025, the world built more coal and used it less. Development has grown more concentrated, too—95% of coal plant construction is now in China and India, and even they are building solar and wind fast enough to displace it."

Shearer further emphasizes that the core issue is no longer technological, but political: "The central challenge heading into 2026 is not the availability of alternatives, but the persistence of policies that treat coal as necessary even as power systems move increasingly beyond it."

Government officials in China and India maintain that coal remains a critical "baseload" fuel necessary to support rapid industrialization and protect against the intermittency of renewables. However, domestic policies in both nations are beginning to reflect the changing reality. China’s latest five-year plan pledges to "promote the peaking" of coal use, and new regulations have introduced stricter controls on local governments regarding the approval of fossil-fuel projects.

Implications: The Long Road to Phase-Out

The implications of this "10-year high" in coal construction are profound.

First, the world is creating a significant amount of "locked-in" carbon emissions. If these 97GW of new plants operate for their full projected lifespans, they will complicate global efforts to meet the Paris Agreement temperature targets. The financial risk is equally significant; as renewables become cheaper and more reliable, these plants may never reach the return on investment originally projected by their developers.

Second, the "disconnect" suggests that the transition away from coal will not be a linear process. It will be characterized by spikes in activity—driven by geopolitical shocks and energy security anxieties—that mask a deeper, structural decline. The "return to coal" that many feared following the Iran war has proven to be limited, suggesting that the global market is now too integrated with renewable technology to fully revert to the coal-reliant models of the past.

Finally, the shift toward clean energy is gaining an irreversible momentum. With solar and wind now the primary drivers of global electricity expansion, the economic argument for building new coal capacity is becoming increasingly tenuous. The next few years will likely be defined by a battle between the political desire to maintain legacy coal infrastructure and the economic imperative to embrace a cheaper, cleaner, and more decentralized energy future.

As the world heads into 2026, the data provides a clear warning: building more capacity will not restore coal to its former dominance. Instead, it creates a fragile energy system, vulnerable to the changing economics of a world that is rapidly leaving the age of coal behind.