Editorial Note: This brief was updated on May 11, 2026, to reflect significant shifts in the Trump administration’s implementation strategy for the BALANCE Model within Medicare and the extension of the Medicare GLP-1 Bridge program through the end of 2027.

The rapid rise of glucagon-like peptide-1 (GLP-1) receptor agonists—a class of drugs revolutionizing the treatment of type 2 diabetes, obesity, and cardiovascular disease—has placed the federal government at a crossroads. While these medications have demonstrated remarkable clinical efficacy, their high price tags and existing statutory coverage limitations have created a massive barrier to access for millions of Americans. As of early 2026, roughly 56% of GLP-1 users reported difficulty affording their prescriptions, with one in four describing the financial burden as "very difficult."

In response, the Trump administration has initiated a multi-pronged strategy to reduce costs and broaden access. These efforts include "most-favored nation" pricing deals with major manufacturers, the launch of the TrumpRx discount portal, and the development of the "Better Approaches to Lifestyle and Nutrition for Comprehensive hEalth" (BALANCE) Model. However, the path to implementation has proven complex, characterized by administrative pivots, industry pushback, and ongoing debates regarding the long-term fiscal sustainability of covering obesity medications.

The Statutory Barrier: A Fundamental Mismatch in Coverage

Current federal law creates a paradoxical environment for patients seeking weight-loss treatment. While Medicare is explicitly prohibited by statute from covering medications specifically for weight loss, the program covers these same drugs when prescribed for medically accepted indications such as type 2 diabetes or cardiovascular risk reduction. This creates a scenario where a patient with obesity can access a GLP-1 if they have secondary comorbidities, but those without such conditions—or those whose providers haven’t documented them—are left to pay the full cash price.

The situation in Medicaid is equally fragmented. Under the Medicaid Drug Rebate Program (MDRP), states are mandated to cover most FDA-approved drugs; however, weight-loss medications are categorized as an optional benefit. Consequently, coverage varies wildly by state. As of January 2026, only 13 states provided coverage for GLP-1s specifically for weight loss, a decrease from 16 states the previous year. This decline highlights the tightening of state budgets and the intense fiscal pressure these drugs place on public coffers.

Chronology of Federal Policy Shifts

The administration’s roadmap for expanding access has undergone significant revision in recent months.

- 2025: The GLP-1 drug semaglutide (marketed as Ozempic, Wegovy, and Rybelsus) was selected for Medicare drug price negotiation, with new, lower prices scheduled to take effect in 2027.

- January 8, 2026: Deadline for drug manufacturers to signal participation in the BALANCE Model.

- April 20, 2026: Deadline for Medicare Part D plan sponsors to submit applications for the BALANCE Model.

- April 21, 2026: CMS announces an indefinite delay in implementing the BALANCE Model within Medicare Part D, citing insufficient interest from plan sponsors.

- May 1, 2026: Launch of the BALANCE Model within the Medicaid program, scheduled to run through 2031.

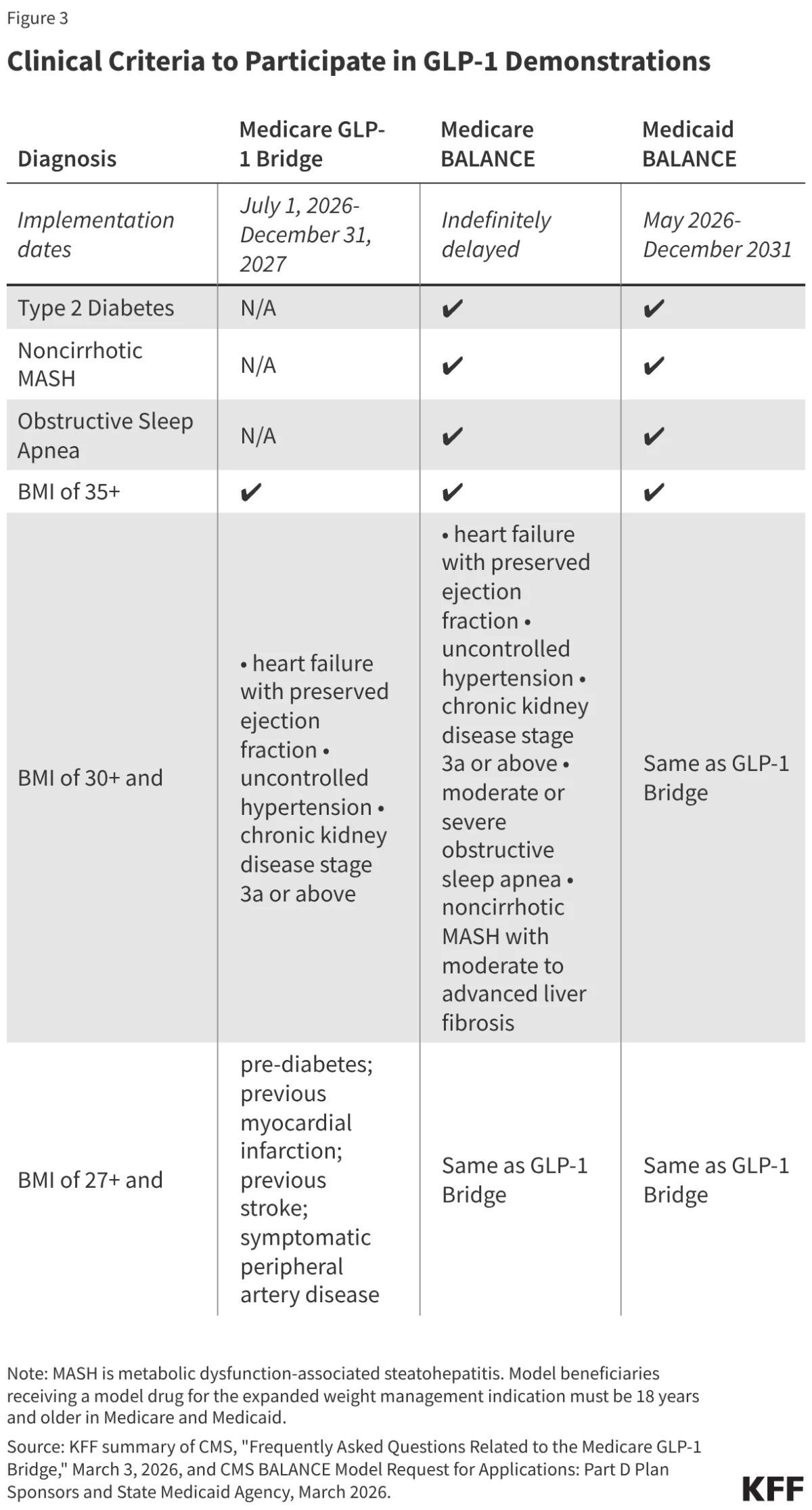

- July 1, 2026: Commencement of the Medicare GLP-1 Bridge program.

- December 31, 2027: New extended expiration date for the Medicare GLP-1 Bridge, which was originally slated to end in 2026.

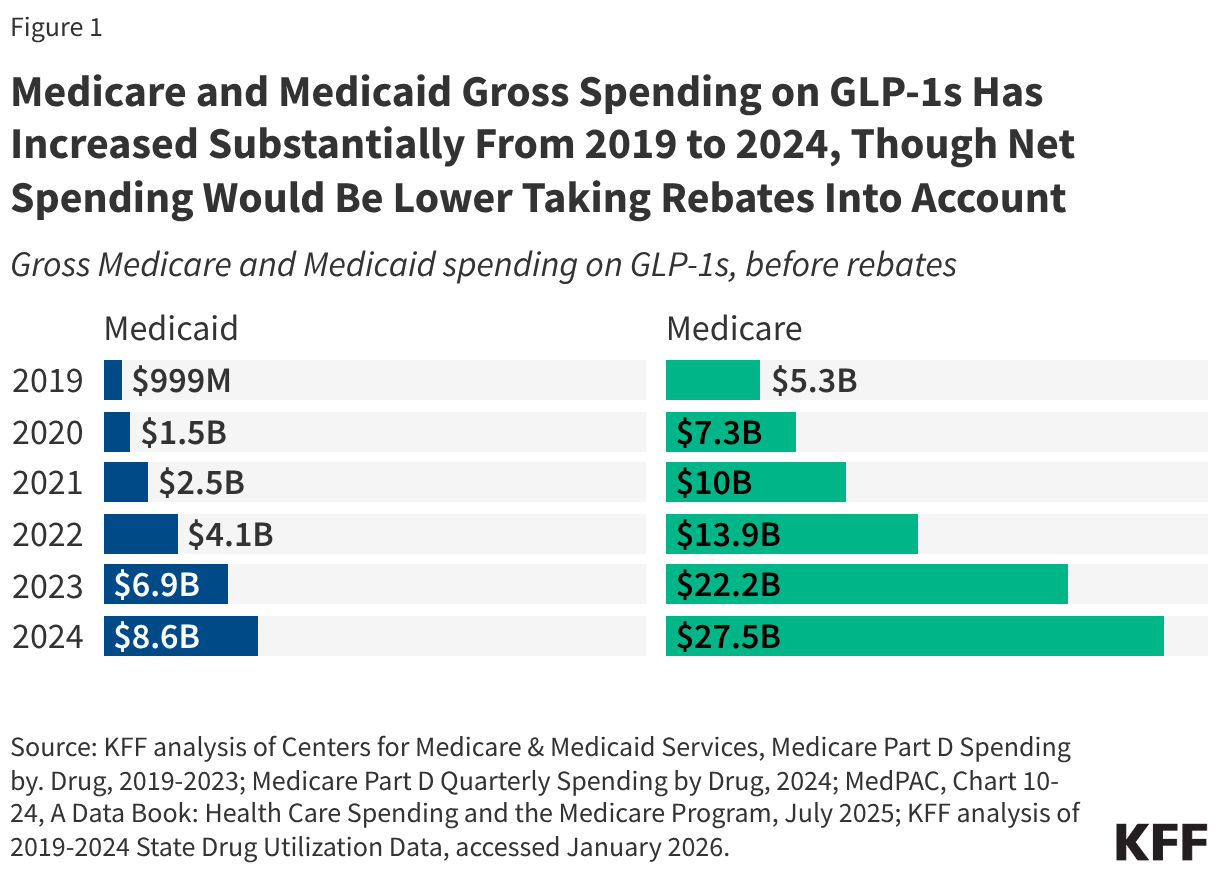

Supporting Data: The Spending Surge

Despite coverage limitations, the utilization of GLP-1s has soared. In 2024 alone, Medicaid recorded 8.4 million prescriptions with $8.6 billion in gross spending. The Medicare program saw an even more dramatic trajectory, with 21.8 million claims and $27.5 billion in gross spending (pre-rebates).

These figures illustrate the "spending trap" facing federal programs: while these drugs offer clear health benefits, the gross cost of widespread adoption for obesity—estimated by some analysts to reach between $25 billion and $35 billion over a decade for Medicare—far outpaces current budgetary provisions. The data confirms that even with the negotiated net prices of $245 per month established by the administration, the sheer volume of potential eligible beneficiaries creates an unprecedented fiscal challenge for both the federal government and participating states.

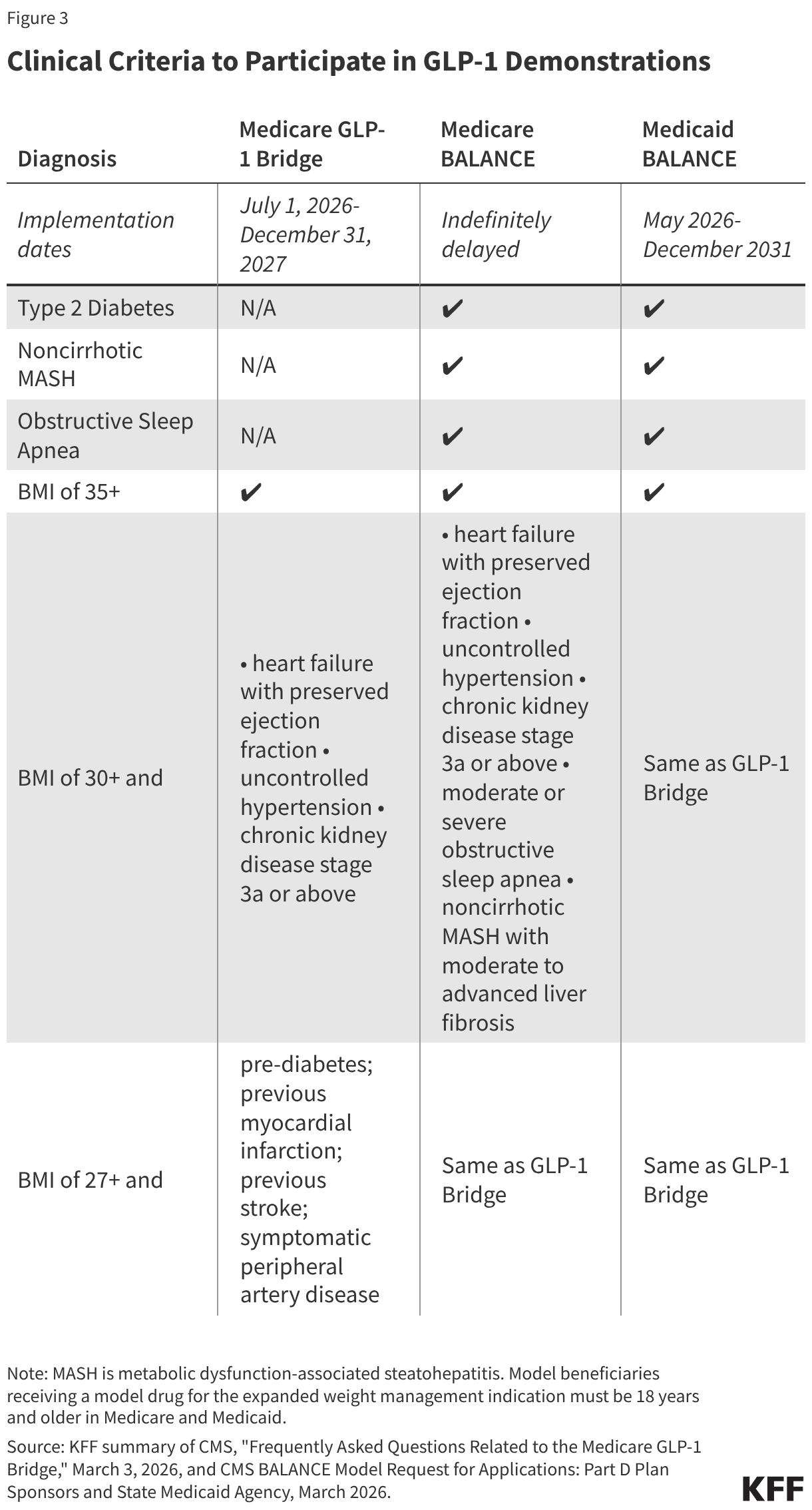

The Medicare GLP-1 Bridge: A Temporary Lifeline

To fill the gap created by the delay of the broader BALANCE Model, CMS is utilizing Section 402 demonstration authority to extend the "Medicare GLP-1 Bridge." This program provides coverage for specific obesity-indicated drugs—including formulations of Foundayo, Wegovy, and the KwikPen version of Zepbound—at a flat $50 monthly copayment.

Crucially, this bridge operates outside the standard Part D benefit structure. This design prevents Part D sponsors from bearing financial risk, which was a key friction point during the BALANCE negotiations. However, this structure also means that the $50 copayment does not count toward a beneficiary’s annual out-of-pocket maximum or deductible, potentially creating a secondary financial hurdle for low-income seniors who may rely on the Low-Income Subsidy (LIS) for other medications.

The BALANCE Model: Design and Discontent

The BALANCE Model was intended to be the centerpiece of the administration’s strategy. Beyond merely subsidizing drug costs, it sought to pair medication with manufacturer-provided lifestyle support programs. These programs were designed to foster healthy eating, physical activity, and medication adherence—elements deemed essential for the long-term success of weight-loss interventions.

However, the voluntary nature of the model became its Achilles’ heel. CMS set an ambitious target: 80% participation among Medicare Part D sponsors. When the April 20, 2026, deadline passed, it became clear that the industry was not prepared to take the leap. Major Part D sponsors expressed concern over the lack of data to accurately model the long-term financial exposure of covering obesity treatments, leading to the indefinite delay of the program in the Medicare sector.

Implications for Stakeholders

For Beneficiaries

The primary impact is uncertainty. While the Medicare GLP-1 Bridge provides a two-year window (2026–2027) of access, there is no guaranteed bridge to permanent coverage. If the statutory prohibition on obesity drugs remains in place and the BALANCE Model fails to gain traction in 2028, patients currently using these drugs could see their access vanish overnight. This "cliff effect" creates significant anxiety for patients who view these medications as medically necessary for their long-term health.

For State Medicaid Programs

The situation is more stable for Medicaid, where the BALANCE Model is moving forward. However, states must weigh the potential for improved public health outcomes against the immediate budgetary hit. While the model offers supplemental rebates, states are still responsible for the underlying costs of expanded eligibility. As seen in the recent decline in the number of states covering these drugs, budgetary constraints may limit the number of states that ultimately sign onto the model by the July 31, 2026, deadline.

For the Healthcare Market

The pharmaceutical industry, specifically manufacturers like Novo Nordisk and Eli Lilly, has shown a willingness to participate, agreeing to the $245 net price point for Medicare. This suggests that while manufacturers are eager to secure a place on federal formularies, the intermediary stakeholders—the insurance plans and state agencies—remain the primary gatekeepers, focused heavily on risk mitigation and long-term cost-predictability.

Conclusion: A Delicate Balance

The Trump administration’s approach to GLP-1 coverage reflects the broader struggle to integrate transformative, high-cost medical breakthroughs into legacy public health systems. The shift from the ambitious BALANCE Model to the more conservative, short-term Bridge program signals an acknowledgment of the industry’s caution.

Whether these drugs will eventually move from "temporary demonstration" status to a permanent fixture of Medicare and Medicaid coverage depends on three factors: the quality of the data collected during the Bridge period, the ability of manufacturers to further lower net costs, and, most importantly, whether clinical evidence of reduced healthcare utilization can eventually justify the initial high investment. Until then, millions of Americans with obesity remain in a state of administrative limbo, caught between a medical innovation that works and a policy framework that has yet to catch up.