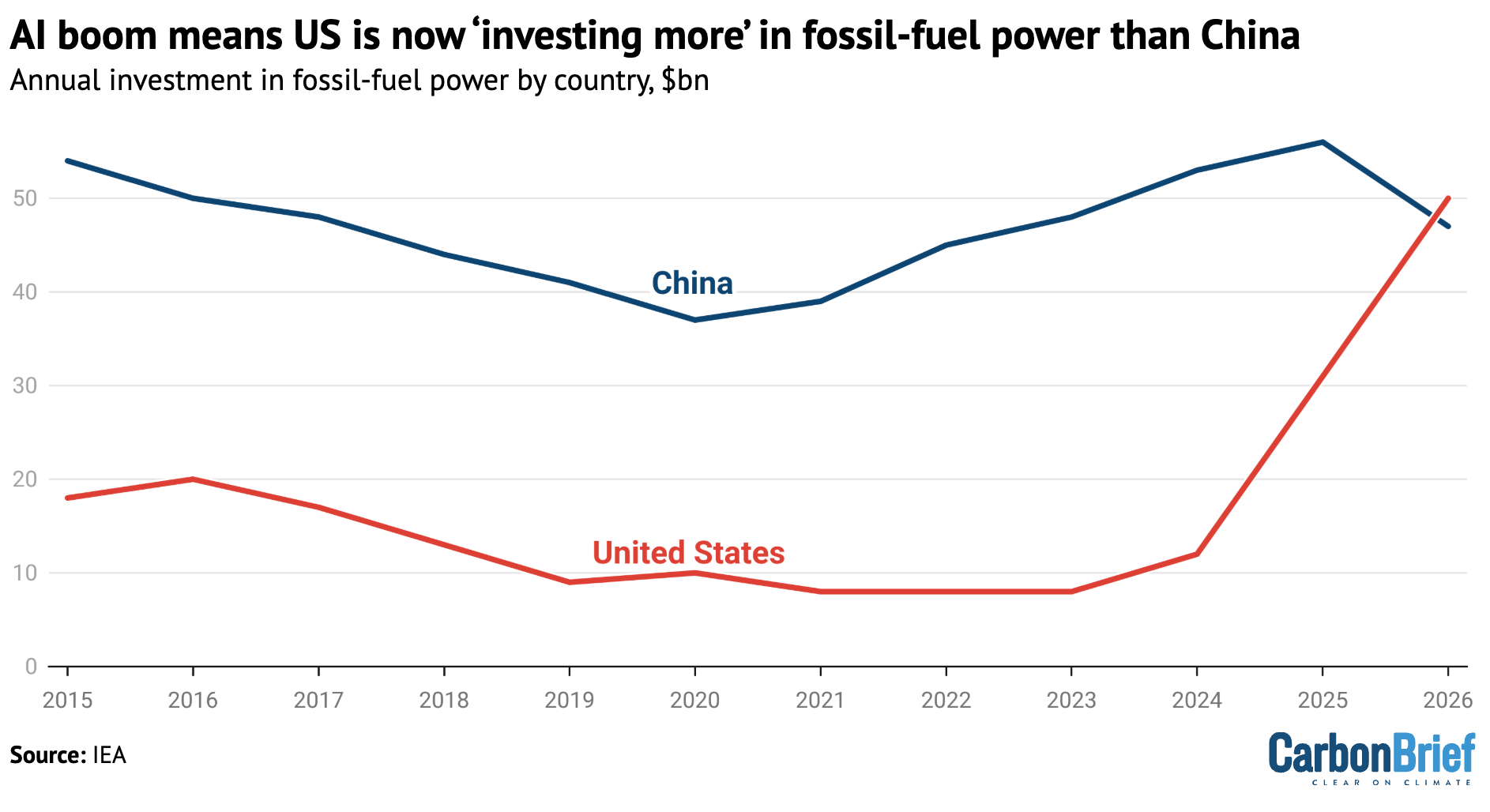

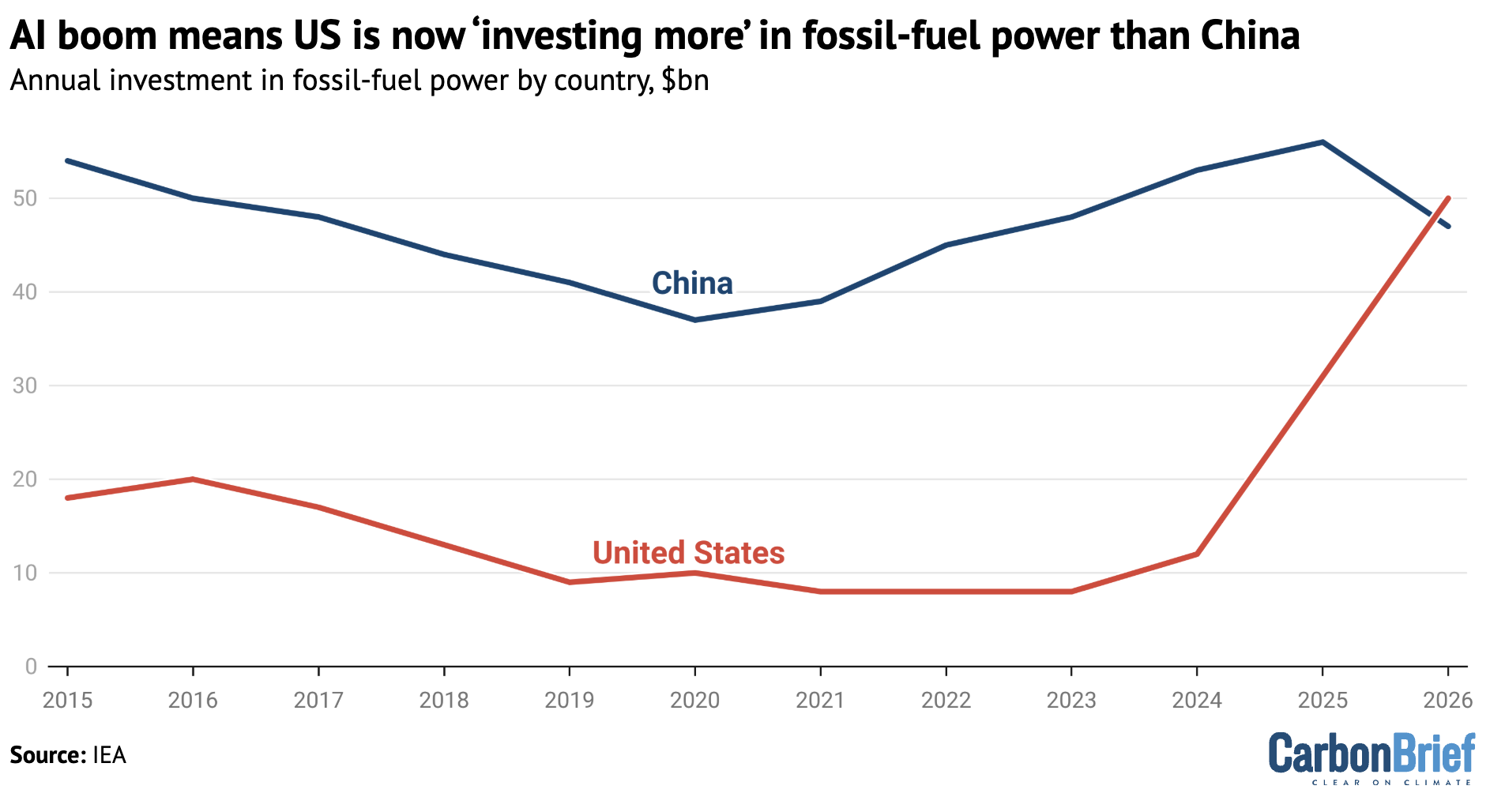

In a dramatic shift that signals a new era for global energy economics, the United States is poised to overtake China in fossil-fuel power investment by the end of 2026. According to the International Energy Agency’s (IEA) latest World Energy Investment 2026 report, this reversal is not driven by a traditional industrial resurgence, but by an unprecedented, AI-led "data-centre boom." As tech giants scramble to secure reliable, high-capacity electricity to maintain dominance in the global artificial intelligence race, they are sparking a massive surge in gas-fired power plant construction, fundamentally altering the trajectory of the energy transition.

The Core Catalyst: The AI Energy Hunger

At the heart of this investment surge is the insatiable power demand of modern artificial intelligence infrastructure. Modern data centres require massive, uninterrupted baseload power, often exceeding the capacity of traditional grid connections. To bypass the bureaucratic delays and congestion associated with public utility upgrades, many major tech companies are pivoting toward "captive" power generation—building dedicated, private gas-fired power plants to ensure their servers remain online around the clock.

This strategy has created a "perfect storm" in the energy sector. Global orders for new gas-power plants soared to 130 gigawatts (GW) in 2025, marking a 25-year high. The IEA identifies the United States—already the world’s largest data-centre market and its primary gas producer—as the "major factor" driving this global acceleration.

A Chronology of the Shift (2025–2026)

To understand the speed of this transition, one must look at the rapid sequence of events over the last eighteen months:

- Early 2025: The AI race hits a fever pitch. Major US tech firms announce massive capital expenditures for new hyperscale data centres. Simultaneously, the supply chain for gas turbines begins to buckle under the sudden demand, leading to a 195% spike in turbine prices due to a supply-demand crisis.

- Mid-2025: US investment in gas-power generation triples. Policy shifts under the Trump administration, including the strategic phase-out of federal tax credits for wind and solar projects, create a vacuum that gas developers move quickly to fill.

- Late 2025: Investment in power infrastructure linked to data centres reaches a staggering $105 billion globally. This single figure highlights the disparity in global capital allocation: the amount spent on fueling AI-driven data centres in a single year now exceeds the total annual energy investment for the entire continent of Africa, where 600 million people still lack basic electricity access.

- Early 2026: As China experiences a cooling in fossil-fuel investment due to shifting national policy priorities and the economic instability caused by the Iran war, the US trajectory continues to climb.

- Projected Late 2026: The IEA projects that for the first time in the modern era, US annual investment in fossil-fuelled power generation will definitively surpass that of China.

Supporting Data: The Anatomy of the Investment

The data provided by the IEA reveals a stark reality. While renewables and grid upgrades remain the dominant focus of global energy spending, the "AI-driven push" is a significant outlier that threatens to derail carbon-reduction targets.

US electricity demand is now expected to grow by an average of 2% per year through 2030. Notably, data centres are responsible for half of this projected increase. The "captive" nature of these developments is particularly significant: since the start of 2025, US-based data centre projects have signed off on more investment in new gas turbines than any sovereign nation on Earth, excluding the United States’ own domestic public utility projects.

The IEA’s market analysis emphasizes that this concentration of demand is having a "crowding out" effect. By soaking up available turbine manufacturing capacity, US data centre developers are effectively limiting the availability of power generation equipment for the rest of the world, creating a bottleneck that hinders energy development in emerging markets.

Policy Shifts and Official Responses

The shift in the US energy landscape is as much a result of policy as it is of technological necessity. The decision to phase out renewable tax credits has forced many corporations to rethink their sustainability portfolios. Where once large-scale wind and solar installations were the primary choice for tech giants looking to "green" their supply chains, the immediate need for reliability in the AI age is tilting the scales back toward fossil fuels.

Industry lobbyists argue that gas is the only viable "bridge" technology capable of meeting the immediate, massive requirements of AI. Conversely, environmental groups have criticized the trend, arguing that it creates a "carbon lock-in" effect, where billions of dollars in new infrastructure will necessitate continued gas consumption for decades to come.

The IEA, while acknowledging the role of gas, points to a secondary, more optimistic trend: the tech sector is becoming a "major energy investor" in its own right. Tech companies now account for 40% of all corporate power-purchase agreements (PPAs) globally. The agency notes that this financial muscle is "underpinning momentum" for emerging, high-risk clean technologies, such as small modular nuclear reactors (SMRs) and advanced geothermal energy, which tech firms view as potential long-term solutions to their power needs.

Implications: A Global Energy Divergence

The implications of the US-China investment reversal are profound.

1. The Reliability vs. Sustainability Trade-off

The US model prioritizes speed and reliability to maintain technological hegemony. However, this comes at the cost of the domestic energy transition. By tethering the AI boom to natural gas, the US is creating a dependency that complicates its long-term climate goals.

2. Global Resource Scarcity

The "turbine crisis" illustrates that global energy infrastructure is a zero-sum game. As the US market absorbs the global supply of critical power-generation hardware to feed its data centres, developing nations are left with fewer options to electrify their own economies. This has sparked concerns regarding energy equity, particularly as the investment gap between tech-hub data centres and energy-poor regions of the world continues to widen.

3. The Rise of the Corporate Utility

We are witnessing the emergence of a new paradigm where "Big Tech" acts as a private utility. By building captive power plants, these corporations are bypassing traditional regulatory oversight and public grid planning. This shifts the power—literally and figuratively—away from national governments and into the hands of a few private entities whose primary motivation is the uptime of their AI models rather than the broader health of the public grid.

4. The Future of Innovation

While the short-term trend is clearly favoring gas, the long-term outlook may hinge on whether tech companies successfully pivot their massive capital reserves into clean baseload technologies. If the current "AI-driven push" can serve as a catalyst for scaling SMRs or next-generation geothermal, it could eventually provide a pathway for the tech sector to shed its reliance on fossil fuels. Until that transition is complete, however, the world remains locked in a high-stakes race where the price of computing power is measured in the output of gas-fired plants.

As the IEA continues to monitor these trends, the narrative is clear: the AI revolution is not just a digital phenomenon. It is a physical one, requiring an massive, earth-moving infusion of power that is currently pulling the world’s largest economies in very different directions.