For millions of young adults across the United States, the traditional milestone of homeownership—once considered the bedrock of the American Dream—is rapidly transforming into a distant, if not unattainable, mirage. A comprehensive new report from the Pew Research Center paints a stark picture of an economy where rising home prices have consistently outpaced the wage growth of those under the age of 40, creating a housing market defined by profound structural inequality.

The data suggests that the barriers to entry are not merely cyclical but are indicative of a deeper, long-term shift in the American economic landscape. As interest rates, property taxes, and insurance costs climb in tandem with home values, the path to building generational wealth through real estate is narrowing, leaving a generation to navigate a precarious landscape of rising rents and stagnant savings.

The Shrinking Horizon: Main Findings

The headline finding of the Pew Research Center’s latest analysis is unambiguous: 89% of adults younger than 40 believe it is significantly harder for young people today to buy a home than it was for their parents’ generation. This sentiment is backed by cold, hard arithmetic. Between 2019 and 2024, the median home price in the U.S. climbed at a rate that far exceeded the growth of household incomes for the same demographic.

This widening gap is best captured by the "price-to-income ratio," a standard metric used to gauge housing affordability. In 2019, the ratio for households headed by those under 40 stood at 2.9. By 2024, that number had surged to 3.5. To put this in historical context, a ratio of 3.5 was last seen during the mid-2000s housing bubble—a period that famously preceded the most significant financial collapse in recent history. For the better part of the late 20th century, that ratio hovered steadily around 2.5.

The implication is clear: the cost of entry has reached levels that historically precede market instability, yet for the average young adult, it represents an immediate and crushing financial barrier.

A Chronology of Economic Erosion

To understand how we arrived at this juncture, one must look at the divergence between housing appreciation and wage stagnation.

In the late 1970s and 1980s, the price-to-income ratio remained relatively stable, hovering between 2.3 and 2.6. During this era, a single-income household could often manage a mortgage, provided they had a modest down payment. However, the trajectory shifted dramatically around the turn of the millennium.

- 2000–2006: The housing market began to overheat, with the price-to-income ratio climbing from 2.5 to a peak of 3.6. This era was marked by loose lending standards, which allowed many to purchase homes they could not technically afford, ultimately culminating in the 2008 subprime mortgage crisis.

- 2010–2019: Following the crash, there was a period of relative "affordability" as prices reset and incomes slowly recovered. In 2019, the ratio was a manageable 2.9.

- 2020–2024: The post-pandemic landscape shattered this stability. Driven by supply chain constraints, a surge in investor interest, and a lack of new inventory, home prices soared. By 2024, the median home price hit $350,000, while the median income for households under 40—adjusted for size—struggled to keep pace, reaching $100,900.

This five-year window has effectively wiped out the gains in affordability seen in the decade following the Great Recession.

Supporting Data: The Anatomy of Unaffordability

The crisis is not just about the sticker price of a home; it is about the total cost of ownership. The Pew study highlights that mortgage rates have undergone a seismic shift, rising from 3.9% in 2019 to 6.7% by 2024.

When you combine a higher purchase price with a significantly higher interest rate, the monthly mortgage payment—coupled with property taxes, property insurance, and private mortgage insurance—has become an impossible hurdle for many. In 2019, 56% of renter households under 40 earned enough to qualify for a mortgage on a median-priced home. By 2024, that figure plummeted to 37%.

Furthermore, the "down payment" remains the most significant psychological and financial barrier. According to a 2024 Federal Reserve survey, 70% of renters under 40 identified the inability to afford a down payment as the primary reason for remaining in the rental market. As home prices rise, the amount required for a standard 20% down payment has ballooned, effectively locking out potential first-time buyers who are already struggling to save while paying high monthly rents.

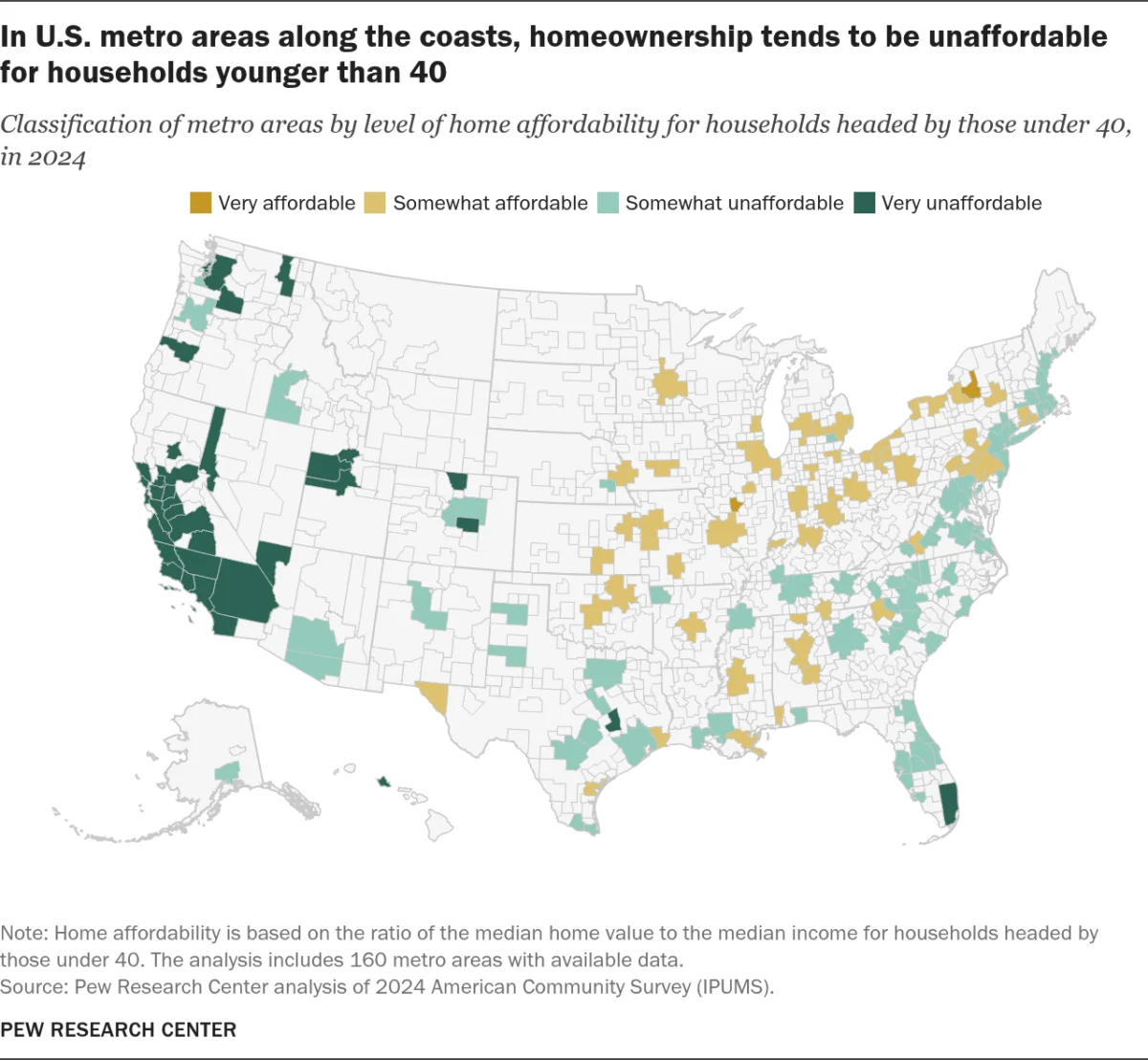

The Localized Crisis: A Tale of Two Geographies

While the national data is concerning, the real story of housing affordability is localized. The analysis of 160 metropolitan areas shows that the decline in affordability is widespread, affecting 142 of those areas.

In 2019, nearly 60% of tracked metro areas were considered "very or somewhat affordable." By 2024, that trend had flipped: 61% of those same areas are now classified as "somewhat or very unaffordable."

Geography is now a primary determinant of economic mobility. The least affordable regions are concentrated heavily along the West Coast and in Hawaii. For instance, in Santa Maria-Santa Barbara, California, the price-to-income ratio is a staggering 9.6. In contrast, the most affordable cities—such as Springfield, Illinois, and Utica, New York—maintain ratios closer to the historical norm of 2.3 to 2.4.

This geographic polarization creates a "mobility trap." Young professionals are often forced to move to high-cost-of-living urban centers for employment, only to find that their salaries, while higher than the national average, are insufficient to bridge the gap between their income and the local cost of real estate.

Official Perspectives and Public Sentiment

The cultural impact of this shift is profound. While 67% of all Americans still view homeownership as a "good investment," the enthusiasm among the younger generation is noticeably dampened. Adults under 40 are less likely to describe homeownership as a "very good" investment compared to their older counterparts.

Experts and policymakers are increasingly divided on the solutions. Some argue for aggressive zoning reform to increase housing density and supply, while others point to the need for federal intervention in the mortgage market or tax incentives for first-time buyers. However, as the data shows, the problem is compounded by a systemic lack of inventory and the financialization of housing, where institutional investors have turned single-family homes into high-yield assets, further squeezing out individual buyers.

Implications for the Future

The inability of a generation to secure housing has wide-ranging societal implications. When young adults cannot purchase homes, they delay household formation, marriage, and childbirth. This ripple effect has long-term consequences for the national economy, including reduced consumer spending in other sectors and a potential crisis in retirement savings, as home equity has historically been a primary vehicle for wealth accumulation among the middle class.

Furthermore, the concentration of unaffordability in coastal states is driving internal migration patterns. People are fleeing places like California for the Midwest or the South, which puts upward pressure on prices in previously affordable regions, potentially exporting the housing crisis to areas that were once safe havens for middle-class families.

Conclusion: A System at a Crossroads

The Pew Research Center’s findings serve as a clarion call. The current trajectory of the American housing market is creating a two-tiered society: those who were able to enter the market before the recent surge, and those who remain on the outside looking in, despite their best efforts to work, save, and plan.

Unless there is a fundamental realignment—through increased supply, innovative financing, or structural policy changes—the dream of homeownership will likely remain a luxury for the few rather than an expectation for the many. For policymakers, the challenge is not just to fix a market, but to restore a sense of economic stability for a generation that increasingly feels as though the ground is being pulled out from beneath them. The statistics are clear; the question that remains is whether the political and economic will exists to reverse the trend before the "price-to-income ratio" reaches a point of no return.