The landscape of American healthcare is currently defined by the massive expansion of Medicare Advantage (MA), a private-sector alternative to traditional Medicare. At the heart of this expansion—and the controversy surrounding its ballooning costs—is the Medicare Advantage Quality Bonus Program (QBP). Established under the Affordable Care Act (ACA), the program was designed to incentivize high-quality care by rewarding plans that achieve a “star rating” of four or higher out of five.

However, as federal spending on these bonuses climbs to record heights, policymakers, researchers, and fiscal watchdogs are increasingly questioning whether these payments genuinely reflect superior patient outcomes or if they have become an expensive, systemic subsidy that lacks clear accountability.

The Mechanics of the Bonus: Incentives vs. Reality

The QBP operates by increasing the “benchmarks”—the maximum amount the federal government pays an MA plan—for those that attain high star ratings. These additional funds are intended to be reinvested into the patient experience, covering supplemental benefits such as vision, dental, and hearing services, or reducing out-of-pocket costs and Part D prescription drug premiums.

While the theoretical goal is to drive quality improvement through competition, critics argue the program is fundamentally flawed. The Medicare Payment Advisory Commission (MedPAC) has repeatedly noted that the current star rating system incorporates too many variables and fails to adequately account for social risk factors that influence health outcomes. Furthermore, because star ratings are reported at the contract level rather than the individual plan level, a single contract may hide wide variations in performance, coverage, and demographic reach across multiple sub-plans.

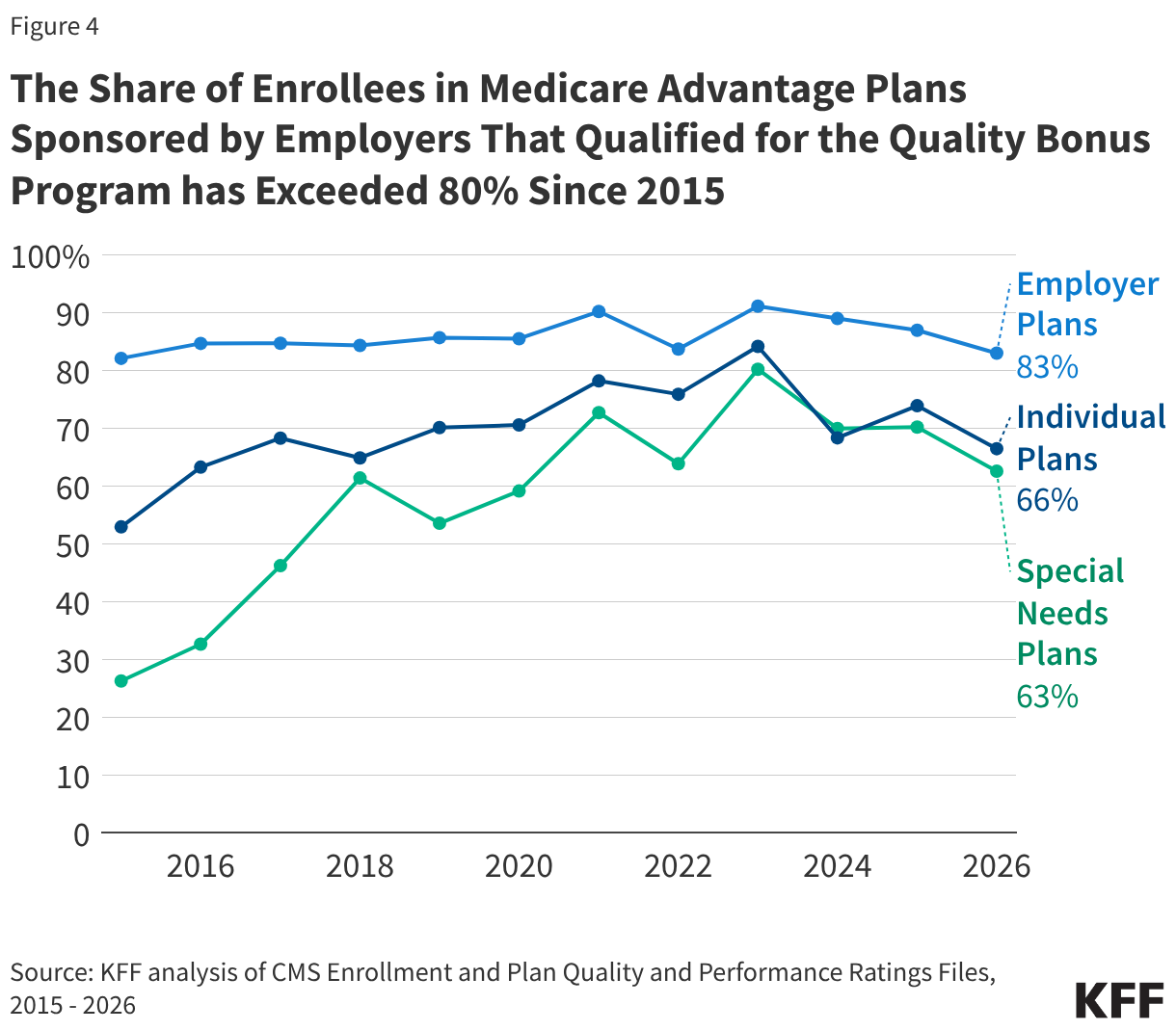

A Decade of Rapid Growth: A Chronology of Escalation

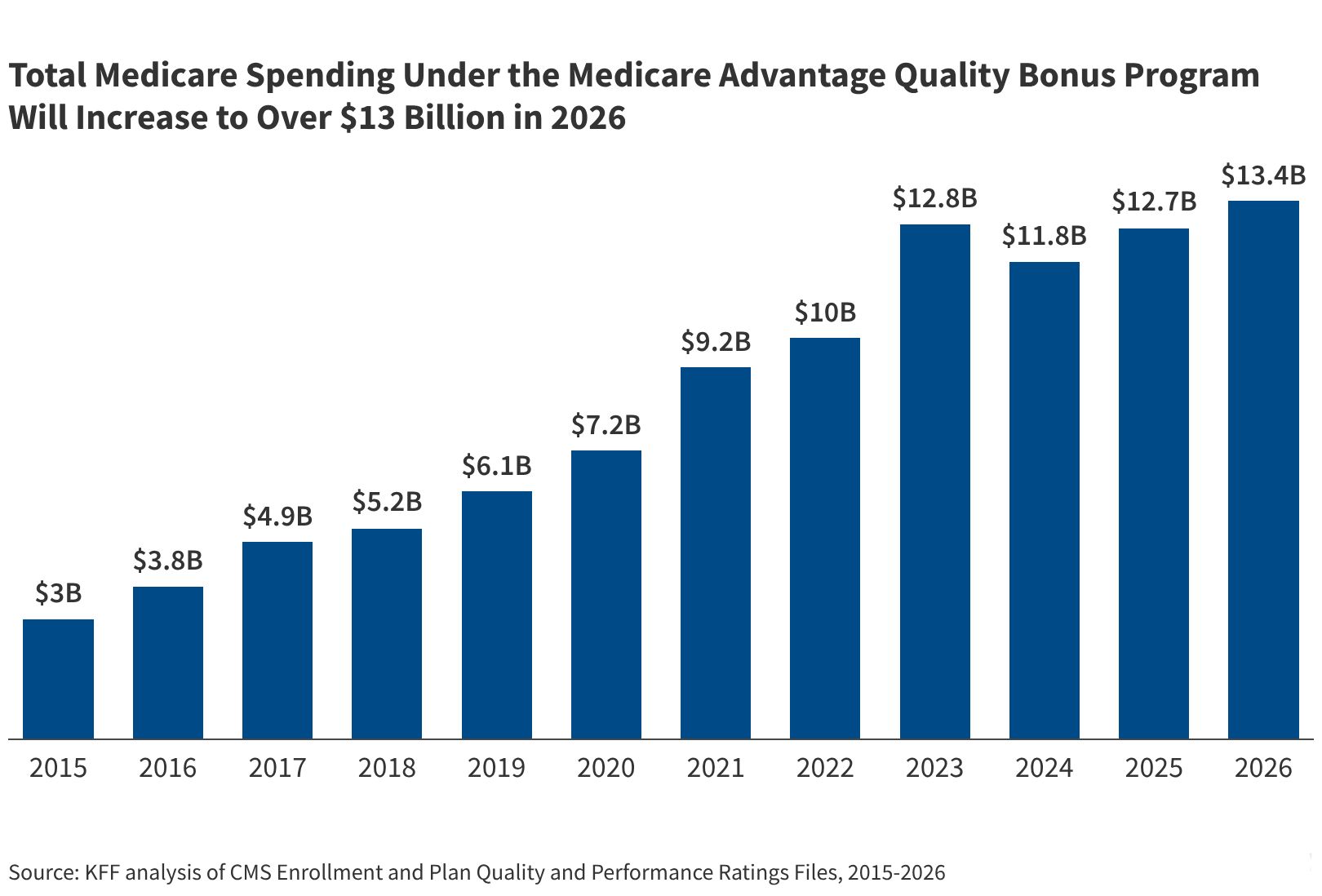

The financial trajectory of the QBP has been nothing short of exponential. In 2015, the program accounted for approximately $3.0 billion in federal spending. By 2026, that figure is projected to hit at least $13.4 billion, reflecting a more than fourfold increase in just over a decade.

Key Milestones:

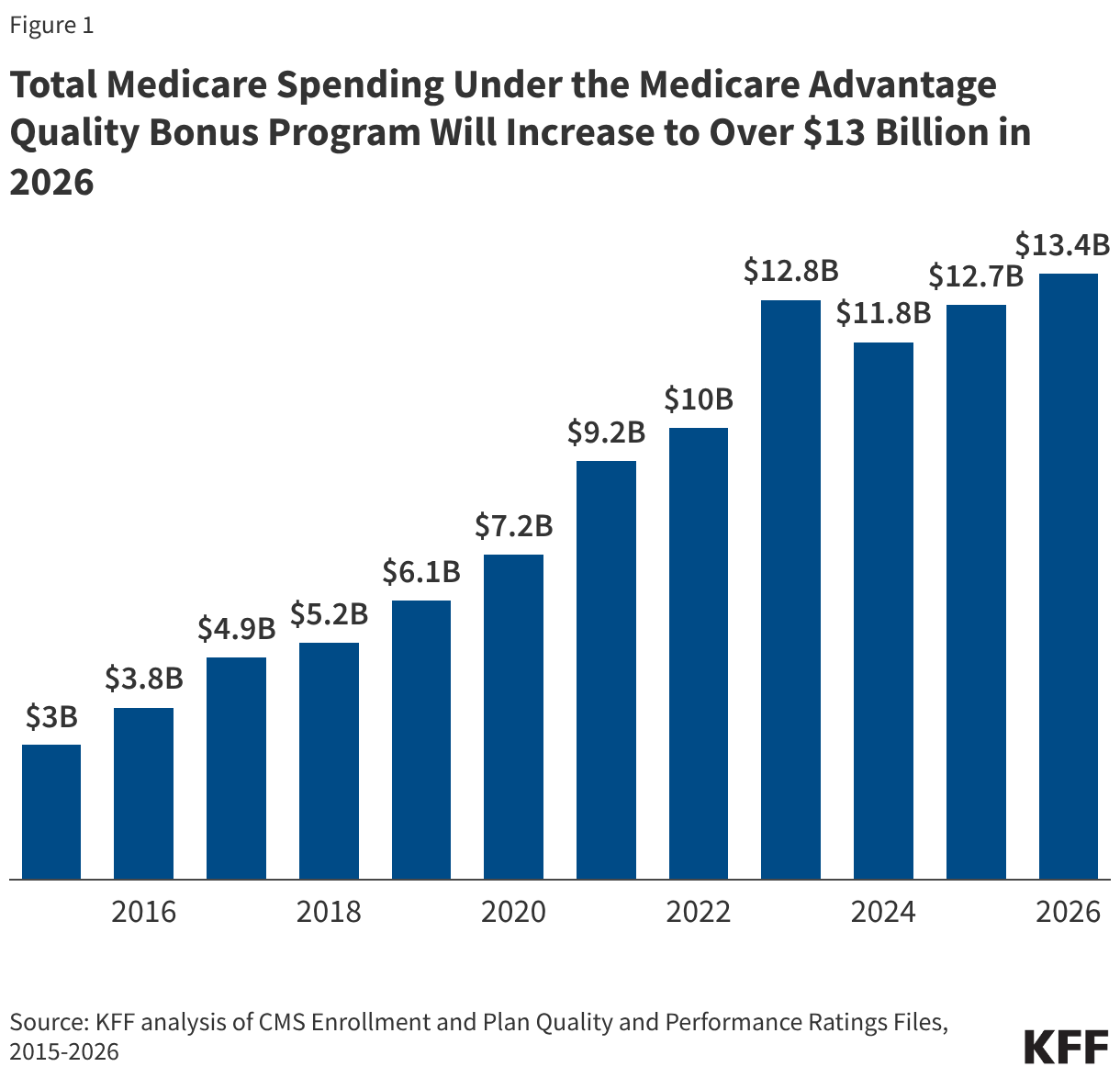

- 2015: The program begins to mature, with roughly 55% of MA enrollees in plans qualifying for bonuses.

- 2018: The Congressional Budget Office (CBO) conducts an analysis suggesting that the elimination of the QBP could save the federal government nearly $100 billion over a decade. Since then, enrollment in MA has surged past even the most aggressive projections, suggesting these savings would be significantly higher today.

- 2023: A peak year for eligibility, with 75% of enrollees in bonus-eligible plans.

- 2026: While the share of enrollees in bonus plans dipped slightly to 68% due to more rigorous CMS scoring, total spending continues to rise, hitting an estimated $13.4 billion—a clear indicator that the cost per enrollee is outpacing enrollment growth.

Supporting Data: Where the Money Goes

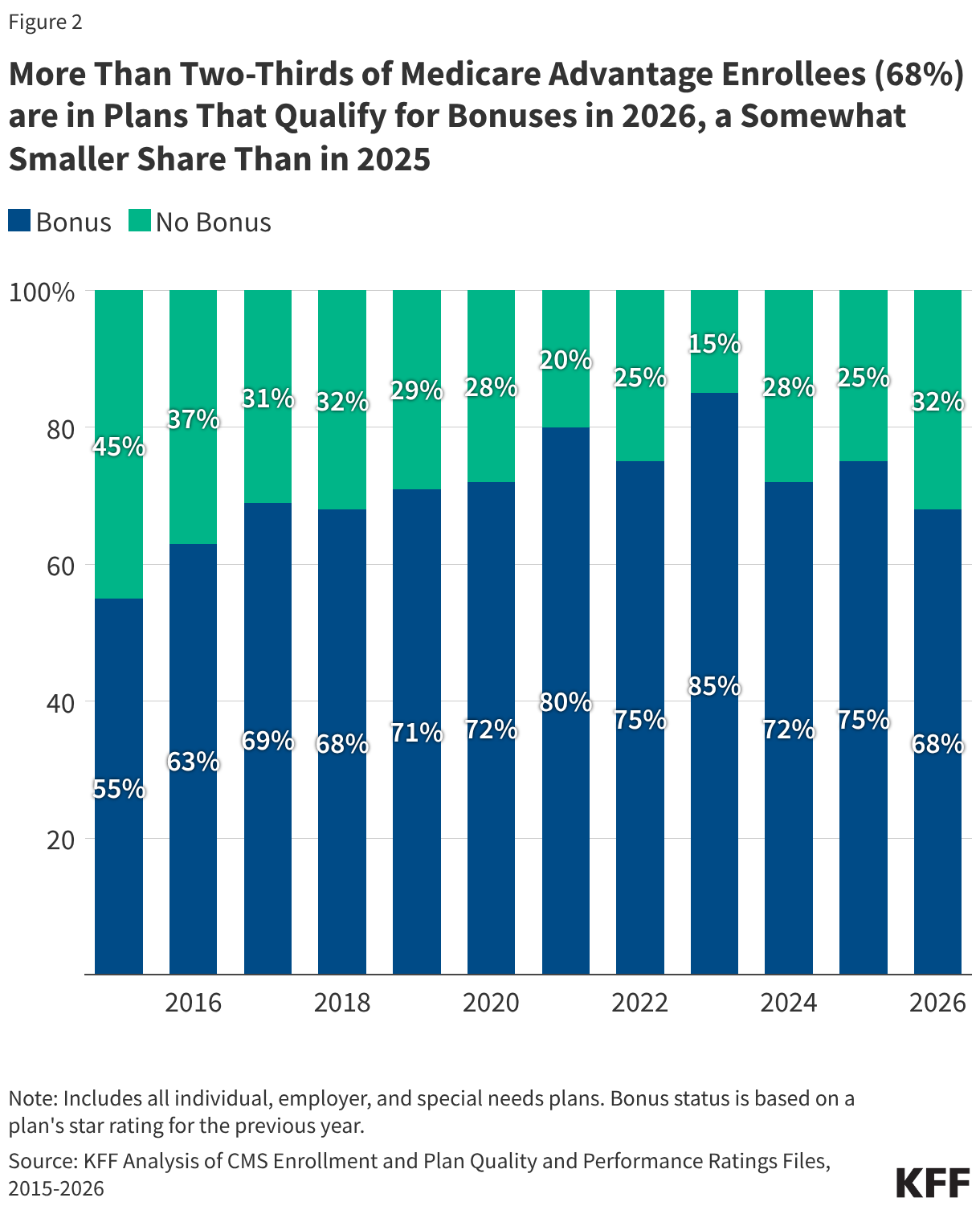

The distribution of these bonus payments is not uniform. Data shows that employer- and union-sponsored MA plans receive significantly higher per-enrollee payments than individual or special needs plans. In 2026, the average annual payment increase for group employer plans stands at $466, compared to $381 for individual plans and $318 for special needs plans (SNPs).

The disparity is largely driven by the high star ratings consistently maintained by employer-sponsored plans. Since 2015, more than 80% of enrollees in these group plans have been covered by bonus-eligible contracts. This raises a critical question for regulators: Are these plans truly providing better care, or is the benefit structure inherently easier to manage because the population is limited to retirees of specific, often stable, organizations?

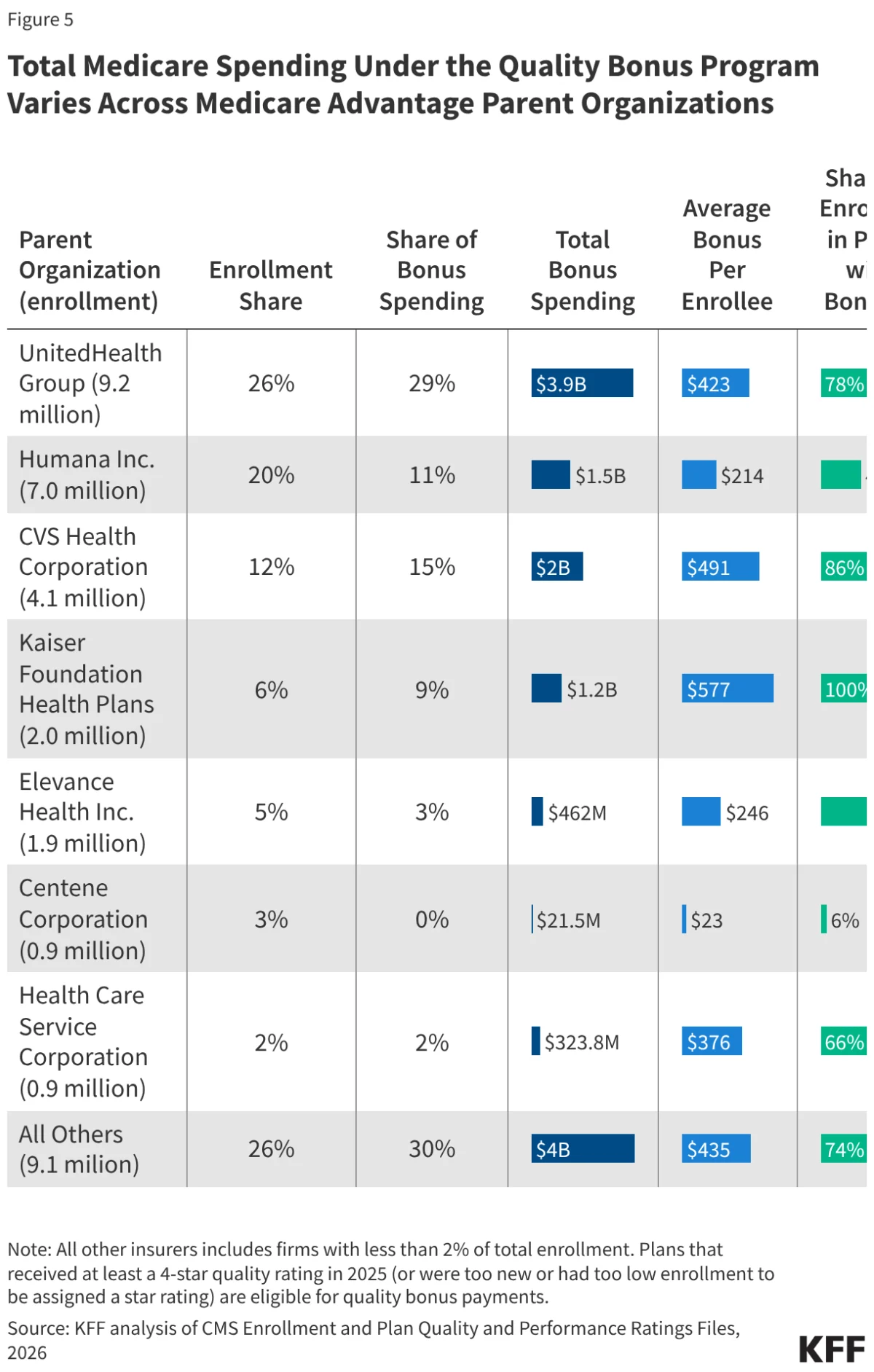

Corporate Concentration

The fiscal impact of the program is highly concentrated among a few major parent organizations. UnitedHealth Group, which commands 26% of the total MA market, is set to receive 29% of all bonus spending—totaling $3.9 billion in 2026. Conversely, Humana, the second-largest player with 20% of the market, will receive a disproportionately smaller share (11%) due to a notable decline in its average star ratings following the 2025 plan year.

Official Responses and Regulatory Turbulence

The Centers for Medicare & Medicaid Services (CMS) has recently attempted to address concerns regarding the complexity and effectiveness of the rating system. In a move finalized for the 2029 star ratings, CMS has opted to remove several administrative measures that no longer effectively differentiate between high- and low-performing plans.

While CMS describes this as a step toward simplification, the move is expected to increase Medicare spending by $18.6 billion over the next decade. The irony is not lost on observers: in attempting to “clean up” the metrics, the government has inadvertently made it easier for more plans to qualify for bonus payments, thereby inflating the total cost.

The industry has responded with both litigation and lobbying. Companies like Humana and Clover Health have engaged in high-profile legal battles against CMS over the methodology used to calculate star ratings. These cases highlight the extreme volatility of the bonus system; when a single star-rating adjustment can result in hundreds of millions of dollars in revenue fluctuations, insurers have every incentive to challenge the government’s math in court.

Implications for the Future of Medicare

The implications of the current QBP structure are profound, particularly as the federal government grapples with long-term fiscal sustainability.

1. The "Coding Intensity" Problem

The reported $13.4 billion in bonus spending is likely a conservative floor. Because the bonus is applied to the benchmark, it interacts with "risk scores"—the diagnostic data used to predict how much care an enrollee will need. As insurers increase their "coding intensity"—a practice of more aggressively documenting patient conditions to raise risk scores—the value of the bonus payment increases correspondingly. MedPAC estimates that when accounting for these inflated risk benchmarks, the actual impact on federal spending is closer to $16 billion annually.

2. Lack of Transparency

There is a persistent "black box" regarding how these bonus dollars are spent. While the program allows insurers to offer extra benefits, there is no requirement for them to disclose exactly how much of the bonus payment is passed on to the beneficiary versus how much is retained as administrative profit or spent on marketing. The lack of transparency regarding employer-sponsored plans makes it nearly impossible to determine if the public is receiving a return on this multi-billion dollar investment.

3. The Need for Structural Reform

The consensus among non-partisan analysts is shifting toward a need for fundamental reform. Options currently on the table range from capping the total bonus pool to entirely decoupling quality bonuses from the benchmark payment system. If the goal is to improve health outcomes, critics argue that the government should reward outcomes directly—such as reduced hospital readmissions or improved management of chronic disease—rather than relying on a star-rating system that incentivizes administrative optimization over clinical success.

Conclusion

As Medicare Advantage continues to grow, capturing a larger share of the federal budget, the Quality Bonus Program stands as a primary target for policy reform. The program was born from a noble intention: to reward excellence in a competitive market. However, with spending quadrupling and questions regarding the validity of the underlying metrics mounting, the program has evolved into a fiscal behemoth.

Whether Congress chooses to reform, replace, or sunset the program will be one of the defining debates of the coming legislative sessions. For now, millions of enrollees benefit from the supplemental services these bonuses provide, but the American taxpayer continues to foot an ever-increasing bill for a system that many experts argue is failing to prove its own worth.