By Financial Policy Desk

On June 9, 2026, the Medicare Board of Trustees released their annual assessment of the program’s financial health, painting a complex picture of a system grappling with rapid growth in specialized medical services, shifting enrollment patterns, and a looming deadline for the Hospital Insurance (Part A) trust fund. The 2026 report serves as a critical diagnostic of the federal government’s largest health entitlement, highlighting how policy decisions, demographic shifts, and the evolving nature of medical care are recalibrating the fiscal trajectory of Medicare.

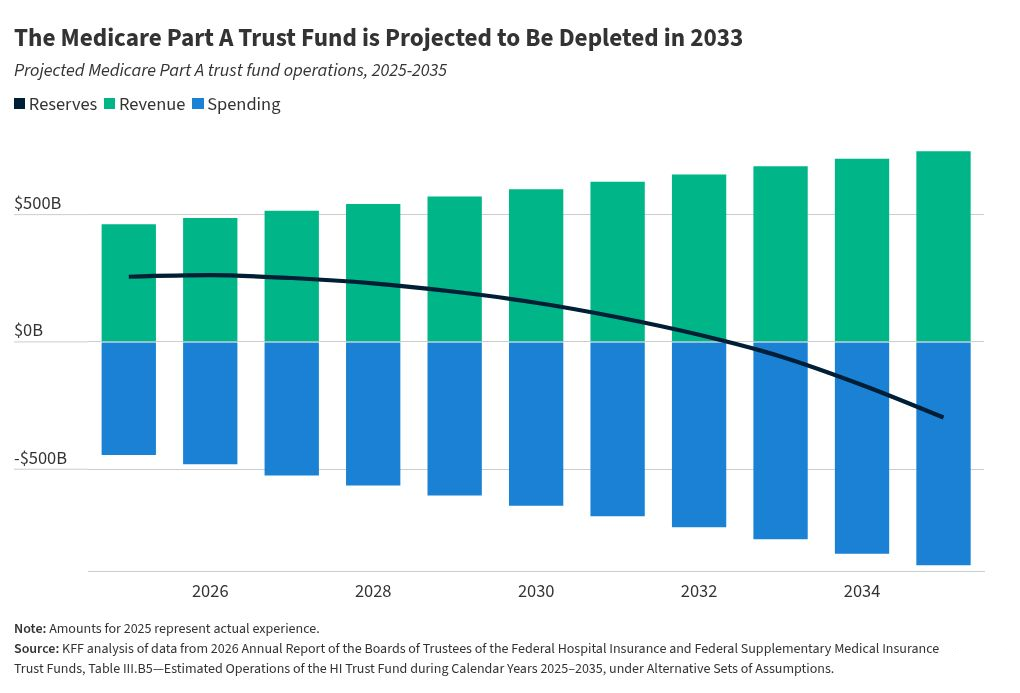

With the Part A trust fund now projected to face depletion in the second quarter of 2033—a timeline that has accelerated by one quarter compared to last year’s projections—policymakers are under mounting pressure to address the structural imbalances inherent in the program.

Main Facts: A System in Transition

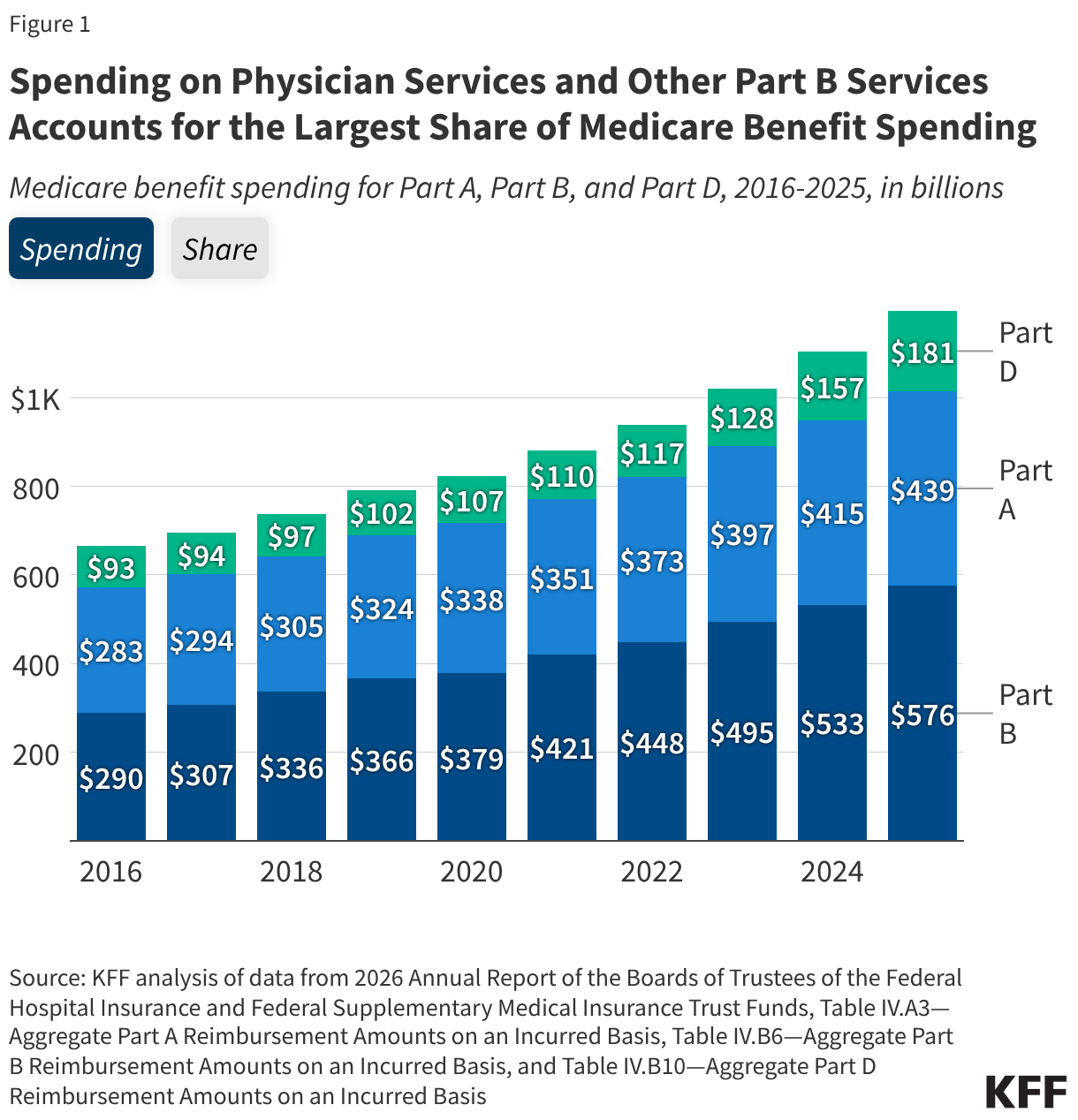

The 2026 report reveals that Medicare benefit payments reached a staggering $1.2 trillion in 2025, nearly double the $666 billion spent just a decade prior. This surge is not merely a product of increased enrollment but a reflection of the rising intensity of medical care and the integration of high-cost specialty pharmaceuticals into the standard of care.

The most pressing headline remains the insolvency of the Part A trust fund. This fund, which covers inpatient hospitalizations, skilled nursing care, and hospice services, relies primarily on payroll tax revenue. According to the Trustees, the primary driver for the accelerated 2033 depletion date is a downward revision in projected Social Security tax revenue, exacerbated by legislative changes introduced in the 2025 budget reconciliation bill (H.R. 1).

When the reserves hit zero, the system will face a "cliff" scenario: without legislative intervention to either increase revenue through tax adjustments or curtail spending through benefit cuts or provider reimbursement reductions, the program would lack the liquidity to cover all promised Part A benefits.

Chronology of Medicare Spending Trends

To understand how Medicare reached this juncture, one must examine the shifts in spending distribution over the last ten years.

- 2015–2016: Part A services, traditionally the backbone of Medicare spending, accounted for over 43% of total benefit expenditures.

- 2016–2025: A clear structural pivot occurred. Spending on Part B—which covers physician services, outpatient procedures, and physician-administered drugs—surged to 48% of total benefits by 2025. During this same window, Part A’s share dropped to 37%.

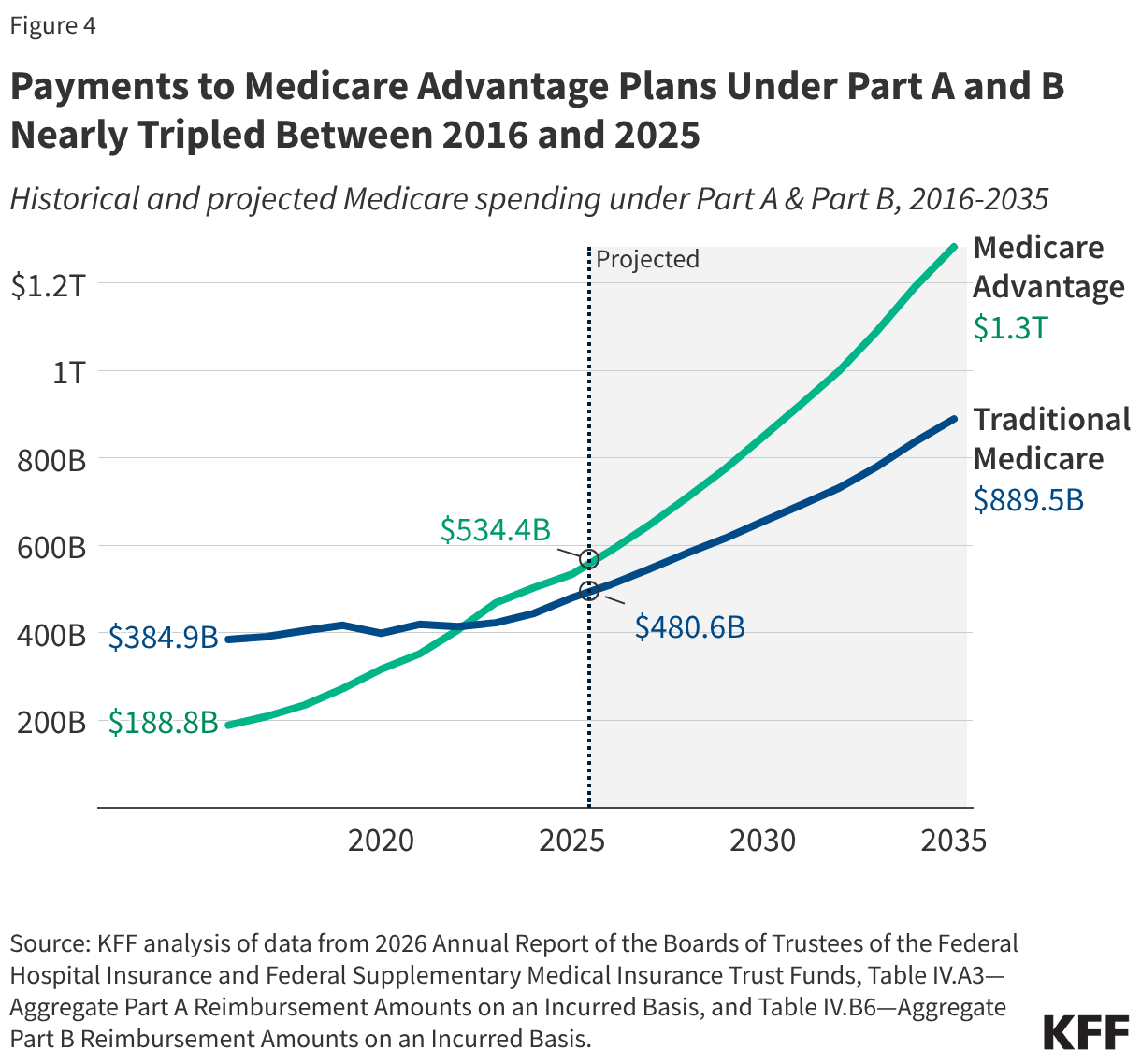

- 2025: Medicare Advantage (MA) reached a historic milestone, accounting for 53% of total program spending. This signifies a dramatic shift from traditional fee-for-service models toward private plan administration.

- 2033: The projected year of insolvency for the Part A trust fund, assuming current trends in tax revenue and expenditure continue.

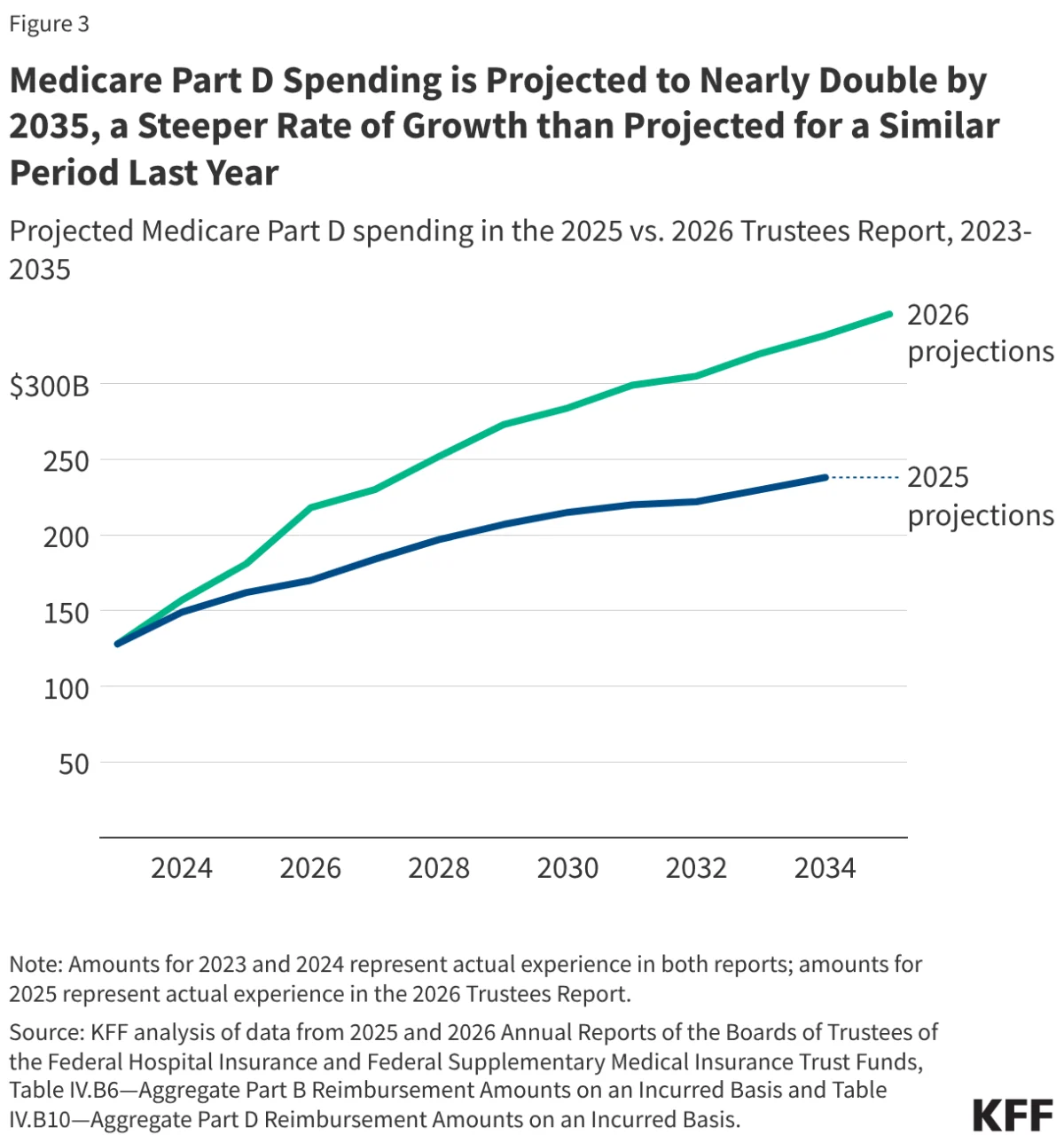

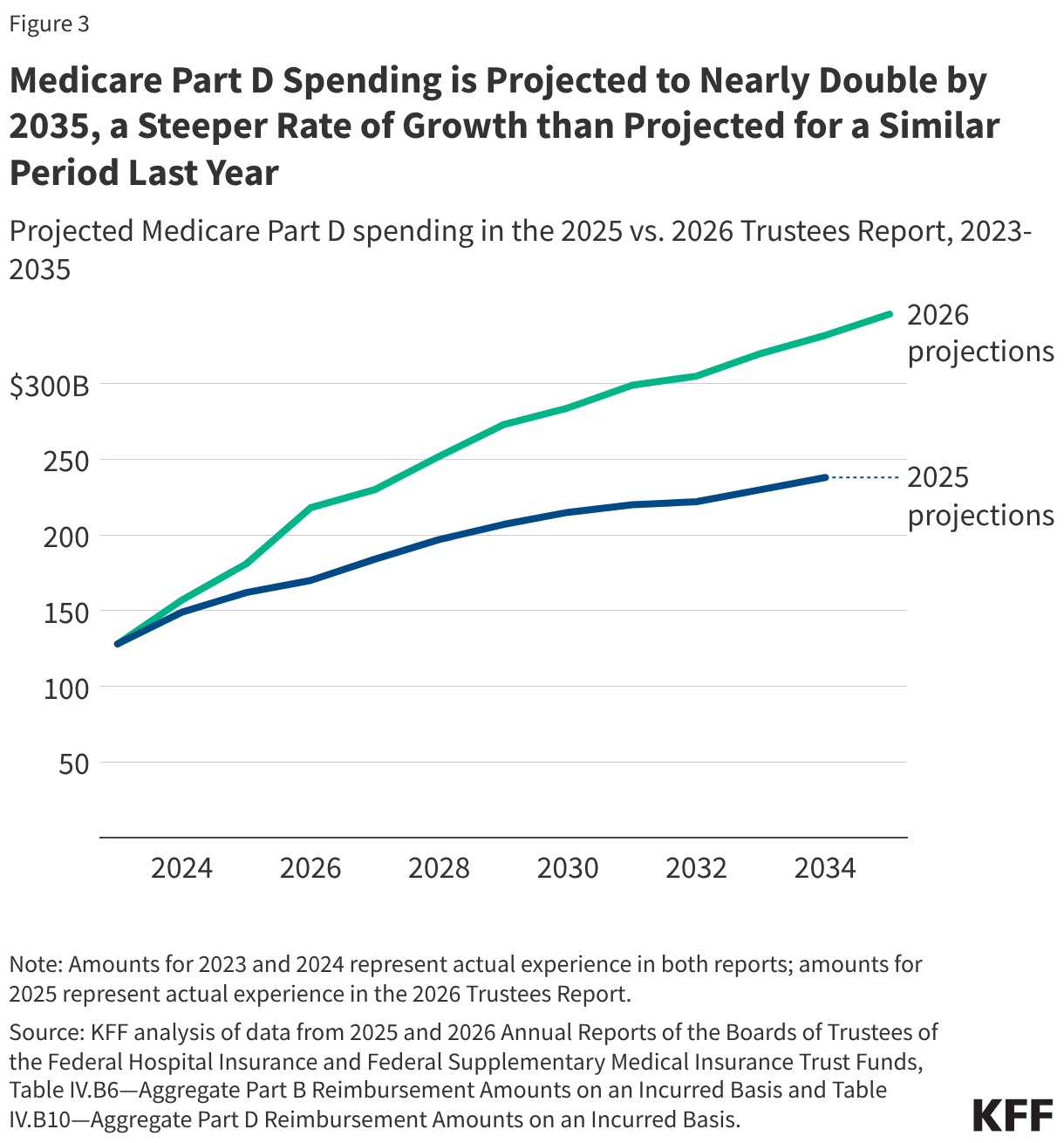

- 2035: The horizon year for the current ten-year forecast, by which time Part D spending is expected to nearly double from current levels.

Supporting Data: The Rising Costs of Care

The 2026 report underscores that Medicare is no longer just a hospital-based program. The shift toward outpatient settings and the emergence of high-cost therapeutics have fundamentally altered the cost structure.

The Part D Prescription Drug Surge

Perhaps the most notable finding is the aggressive growth trajectory for Part D. The Trustees now project spending to climb from $181 billion in 2025 to $346 billion by 2035. This represents an average annual growth rate of 6.7%, significantly higher than the 4.8% forecasted in previous reports. The culprit? The widespread adoption of GLP-1 agonists and other high-cost specialty drugs. Furthermore, the redesign of the Part D benefit, while beneficial to beneficiaries in terms of coverage generosity, has increased the federal government’s share of liability, effectively transferring more financial burden to the taxpayer.

The Medicare Advantage Dominance

The growth of Medicare Advantage is perhaps the most significant structural change in the program’s history. With 54% of eligible beneficiaries now enrolled in private plans, federal payments to these entities have tripled over the last decade. However, the report highlights a growing "efficiency gap": the federal government pays roughly 14% more per enrollee in Medicare Advantage compared to traditional Medicare. This $76 billion "excess" cost is attributed to complex coding intensity and favorable selection, where healthier individuals may gravitate toward private plans, leaving the higher-cost, chronically ill population in the traditional fee-for-service pool.

Official Responses and Legislative Context

The 2026 report serves as a direct feedback loop for the 2025 budget reconciliation bill (H.R. 1). The Trustees specifically cite the bill’s impact on revenue and price negotiation. While the Inflation Reduction Act’s drug price negotiation and inflation rebate provisions are providing some downward pressure on costs, these savings are being offset by other legislative priorities.

The exemption of additional "orphan drugs" from price negotiation, as codified in H.R. 1, is noted by the Trustees as a primary factor in lower-than-anticipated federal savings. This creates a tension between the goal of incentivizing rare disease research and the goal of maintaining Medicare’s long-term solvency. The Trustees’ report suggests that the "generosity" of the new Part D benefit structure, while lauded by patient advocacy groups, carries a significant, long-term fiscal price tag that the current revenue streams are not equipped to handle.

Implications: The Burden on the Beneficiary

The most direct impact of these macro-trends is felt in the household budgets of the elderly. Medicare is not "free"; it is a contributory system where premiums and deductibles are indexed to program costs.

Rising Premiums and Deductibles

The report projects a steady, upward march for out-of-pocket costs. By 2027, the monthly Part B premium is expected to rise to $210, a 3.3% increase over the 2026 rate. When compounded with the rapid 9.7% hike seen between 2025 and 2026, the cumulative effect is significant.

For the average retiree, these costs represent a growing share of fixed income. With seven million beneficiaries already spending more than 10% of their total income on Part B premiums alone, there is growing concern that the program is approaching an affordability threshold.

The "Private vs. Traditional" Divide

Beneficiaries are increasingly forced to choose between the cost-sharing structures of traditional Medicare and the potentially lower, but more restricted, network structures of Medicare Advantage. As MA plans continue to capture a larger share of the market, the traditional Medicare pool may face "adverse selection," where the sicker, more expensive beneficiaries remain in the public program, further straining its financial reserves and potentially necessitating even higher premiums for the remaining participants.

Conclusion: A Call for Structural Reform

The 2026 Medicare Trustees Report is a clear signal that the program’s current financial path is unsustainable. While the insolvency date of 2033 may seem distant to some, the underlying drivers—increased reliance on high-cost outpatient drugs, the persistent payment gap in Medicare Advantage, and the softening of revenue from payroll taxes—require immediate, bipartisan attention.

As the program matures and the "baby boomer" demographic continues to transition into full eligibility, the federal government faces a tripartite challenge: maintaining the quality of care, ensuring the affordability of premiums for a vulnerable population, and guaranteeing the long-term solvency of the trust funds that provide the foundation for American healthcare in retirement. The 2026 report confirms that without structural adjustments, the system will eventually force a choice between significant tax increases or substantial, and potentially painful, benefit reductions.